Predicting Fixed Income Performance through Data-Driven Liquidity Modelling

Introduction

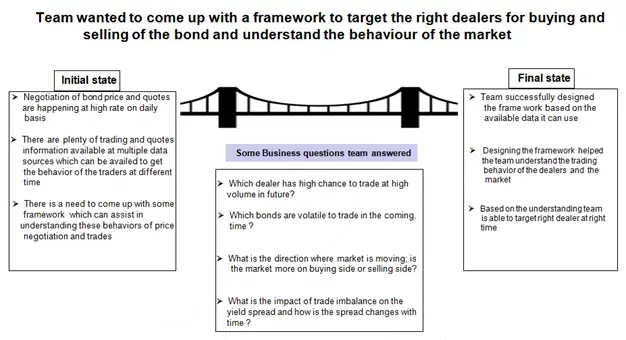

In fixed income markets, liquidity is everything. It determines how easily a bond can be traded without affecting its fair value, a crucial factor for traders, asset managers, and investors alike. Yet despite its importance, liquidity remains one of the hardest metrics to quantify accurately.

A leading global asset management firm partnered with NuWare’s Data Science team to solve this challenge. The objective was to build a predictive liquidity model capable of identifying which bonds were most likely to trade efficiently and when, allowing portfolio managers to buy and sell at the right time and with greater confidence.

By combining deep financial domain expertise with advanced analytics, NuWare developed a Fixed Income Liquidity and Trade Propensity Model that transformed how the client evaluated bond performance and market behaviour.

The Challenge

The client’s fixed income trading desk faced several key limitations in their existing liquidity assessment process:

1. Lack of a Standardized Liquidity Metric

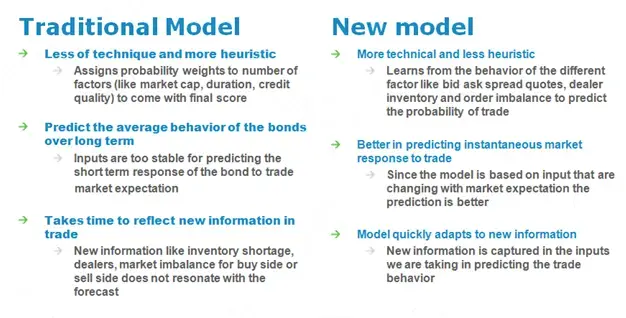

The finance industry lacks a universally accepted formula for liquidity. Each institution uses its own proxies, leading to inconsistent valuations and unpredictable trading behavior.

2. Fragmented and Delayed Insights

Traditional liquidity scores were backward-looking and failed to reflect real-time market dynamics, limiting traders’ ability to act quickly.

3. Opaque Performance Drivers

The client’s existing models could not clearly explain why certain bonds underperformed in liquidity terms, leaving decisions heavily dependent on manual interpretation.

4. Limited Predictive Capability

The models in use did not anticipate future bond performance or volatility, which made proactive trading strategies difficult to execute.

The client needed a robust, data-driven model that not only measured liquidity but also predicted the likelihood of trade success under different market conditions, giving traders an informational edge.

NuWare’s Approach

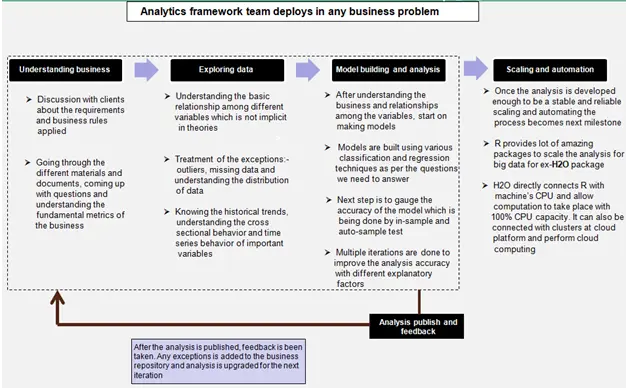

NuWare designed a comprehensive analytical framework grounded in data science and fixed income market behavior. The solution was developed using the DIPP Framework, Descriptive, Inquisitive, Predictive, and Prescriptive analytics, to ensure holistic insight generation.

1. Data-Driven Liquidity Scoring

The team began by leveraging daily transaction data for each bond security. This included trade frequency, volume, price movement, and bid-ask spreads, all indicators of market depth and ease of trade.

Each bond was then assigned a liquidity score, a quantitative measure reflecting its propensity to trade efficiently without price distortion.

2. Factor-Based Analysis

To deepen interpretability, NuWare analyzed multiple attributes that govern bond liquidity:

• Market capitalization

• Coupon rate

• Maturity period

• Issuer credit rating

• Trading frequency and spread behavior

These factors were engineered into a comprehensive feature set, allowing the model to understand how each parameter influences trading dynamics.

3. Predictive Modeling

A machine-learning-based time-series model was built to capture the evolving behavior of each bond over time. Using historical trade patterns and factor relationships, the model predicted the future performance and trade readiness of each security.

4. Model Validation and Testing

To ensure accuracy and robustness, the team conducted:

• In-sample and out-of-sample testing to verify predictive strength

• Scenario and stress testing to assess performance under extreme market conditions

• Backtesting against historical liquidity scores to validate real-world applicability

These steps ensured that the model could generalize across market cycles and asset classes with confidence.

Outcomes

The deployment of the Fixed Income Liquidity Model produced measurable and strategic benefits for the client’s trading and investment operations:

1. Superior Liquidity Insights

The new model provided granular transparency into how each factor, such as coupon rate or credit rating, influenced liquidity, outperforming legacy scoring systems.

2. Predictive Trading Intelligence

Traders gained the ability to anticipate bond performance under varying market conditions, identifying ideal buy and sell windows with greater accuracy.

3. Volatility Forecasting and Risk Control

The model’s predictive analytics enabled early detection of liquidity shocks and price frictions, allowing proactive hedging and risk mitigation.

4. Increased Confidence and Efficiency

Portfolio managers could now base trading decisions on empirical, data-driven signals rather than heuristics, improving both execution speed and confidence.

5. Transparent Performance Metrics

The model provided explainable insights and metrics that could be easily shared with compliance and investment committees, fostering trust in its recommendations.

Compared to the client’s previous model, NuWare’s solution demonstrated higher predictive accuracy, broader factor coverage, and faster analytical turnaround, setting a new benchmark for fixed income analytics.

Future Outlook

Building on this success, NuWare and the client are exploring several avenues for enhancement:

• Integration with Market Data APIs to achieve near real-time updates of liquidity scores.

• Adaptive Learning Models that continuously recalibrate based on evolving trading conditions.

• Cross-Asset Extension to apply the framework across credit derivatives and ETFs.

• Visualization Enhancements with interactive dashboards for scenario-based simulations.

These initiatives aim to transform the liquidity model into a real-time decision intelligence platform for the firm’s fixed income division.

We use cookies to improve your browsing experience on our website, to show you personalized content, to analyze our website traffic, and to understand where our visitors are coming from. By browsing our website, you consent to our use of cookies. Our cookies do not collect personal information. Thank you for your patience.